Resumo A inexistência de um modelo padronizado para a apresentação das demonstrações financeiras dificulta sua análise por parte dos stakeholders, designadamente dos resultados financeiros, em virtude da flexibilidade existente na...

moreResumo

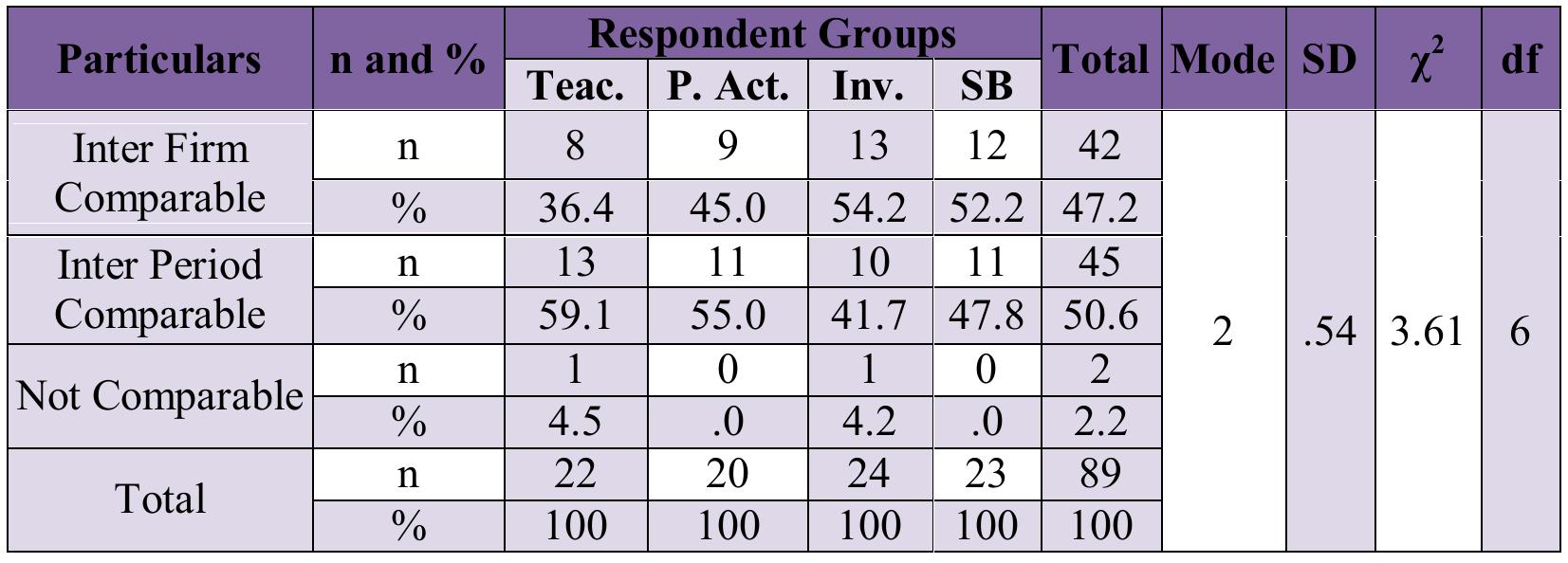

A inexistência de um modelo padronizado para a apresentação das demonstrações financeiras dificulta sua análise por parte dos stakeholders, designadamente dos resultados financeiros, em virtude da flexibilidade existente na International Accounting Standards (ias) 1. Perante esta premissa, questiona-se a possibilidade de comparar demonstrações financeiras entre distintas entidades sem o recurso a ajustamentos adicionais e casuísticos. No sentido de contribuir para a discussão em torno da temática, este estudo analisa o grau de detalhe e os fatores determinantes da apresentação dos itens de gastos e rendimentos financeiros reportados na face da demonstração dos resultados por natureza. Os dados foram recolhidos através dos relatórios e contas consolidados das entidades cotadas no Euronext Lisboa nos anos de 2005, 2010 e 2015, totalizando 118 relatórios ao longo desse período. Foram criados índices de apresentação para possibilitar a analise através de testes bivariados (Mann-Whitney-U). Os resultados sugerem que um conjunto ainda expressivo de determinantes respondem pelos diferentes níveis de detalhe divulgados na demonstração dos resultados em matéria de gastos e rendimentos financeiros, nomeadamente a auditoria externa, a rendibilidade, a normalização contabilística, o período de relato (parcialmente) e a apresentação do resultado financeiro.

Abstract:

The lack of a standardized model for the presentation of the financial statements makes it difficult for stakeholders to analyze them, particularly for financial results, due to the flexibility prescribed by the International Accounting Standards (ias) 1. Given this, the possibility of comparing financial statements amongst different entities without the use of additional and casuistic adjustments is questioned. In order to contribute to the discussion around this theme, this study analyzes the degree of detail and the determinants of the presentation of items of expenses and financial income reported in the face of the income statement by nature. Data were collected through the consolidated reports and accounts of entities listed on Euronext Lisbon in the years 2005, 2010 and 2015, comprising 118 reports during that period. Presentation indices were created to allow the analysis through bivariate tests (Mann-Whitney-U). The results suggest that a still significant set of determinants respond to the different levels of detail disclosed in the income statement for financial expenses and income, namely the external auditing, profitability, accounting standardization, the reporting period (partially) and the presentation of the financial result.