{kind=link}

580 California St., Suite 400

San Francisco, CA, 94104

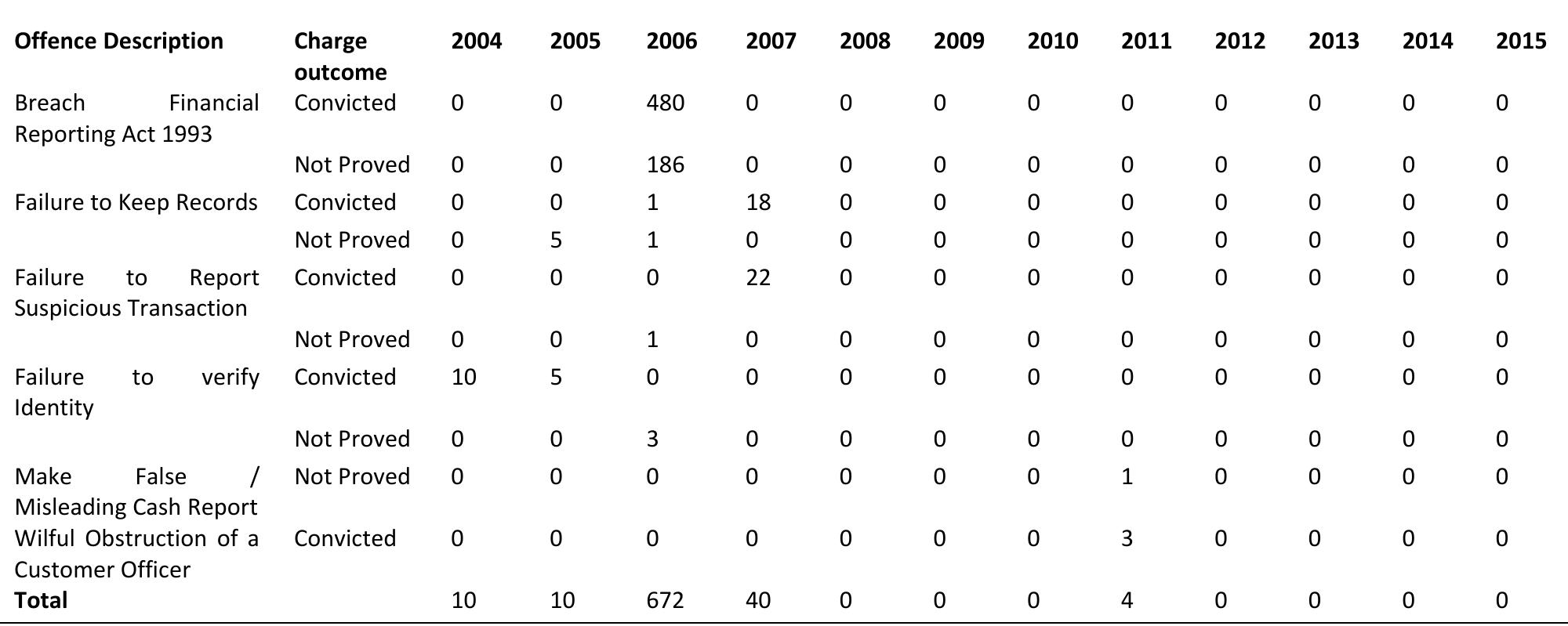

Table 1 Number of Charges Under the Financial Act 1993 and the Financial Transaction Reporting Act 1996 against Corporations, by charge outcome The reduction in financial reporting offences could be attributed to greater financial reporting transparency that exists in IFRS requirements and the limited chances for acquiescence, compromise, avoidance and manipulation of accounting items when enforced (Oliver, 1991). The reduction in the occurrence of charges and convictions associated with financial reporting could also be due to awareness by preparers of financial statements about the regulatory deterrence.