Global Concrete Repair Mortars Market By Product Type (Polymer Modified Cementitious (PMC) Mortars and Epoxy Based Mortars), By Method (Hand/Troweling, Pouring, and Spraying), By Grade (Structural and Non-Structural), By End Use (Building And Carparks, Road Infrastructure, Utility, and Marine), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: May 2026

- Report ID: 185724

- Number of Pages: 296

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

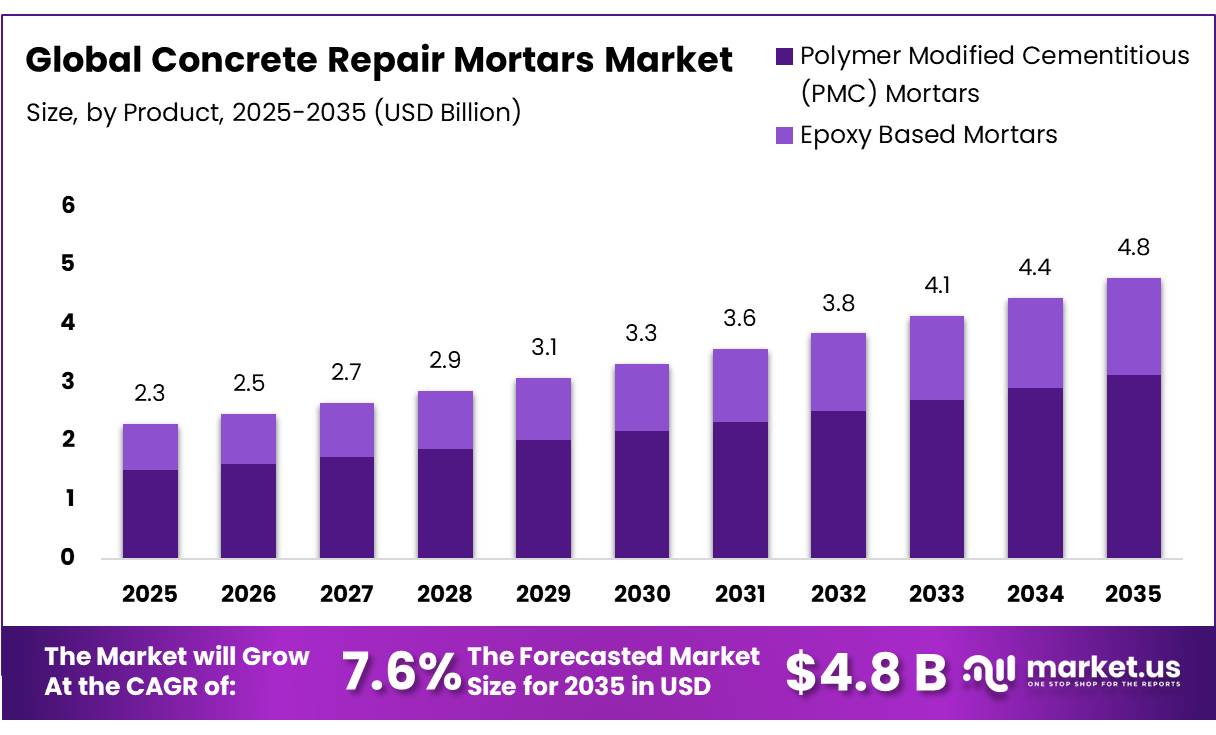

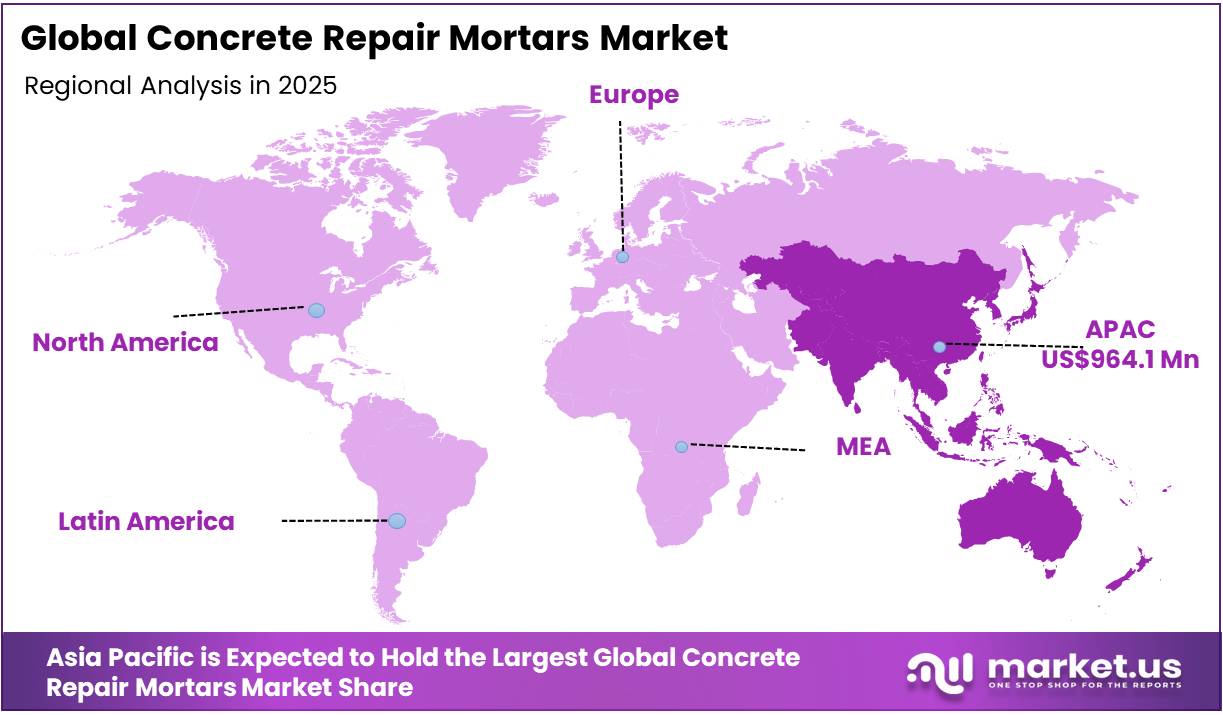

The Global Concrete Repair Mortars Market size is expected to be worth around USD 4.8 Billion by 2035, from USD 2.3 Billion in 2025, growing at a CAGR of 7.6% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 41.2% share, holding USD 278.4 Million revenue.

The concrete repair mortars market is shaped by increasing reliance on rehabilitation solutions to extend the service life of deteriorating concrete infrastructure. These materials are engineered to restore structural integrity and durability in damaged concrete elements affected by cracking, spalling, corrosion, and environmental exposure. Demand is strongly supported by aging bridges, highways, buildings, and marine structures, where full replacement is often impractical due to cost and operational disruption.

Polymer-modified cementitious mortars dominate product usage due to their balanced strength, workability, and cost efficiency, while epoxy-based systems serve more aggressive exposure conditions requiring higher chemical resistance. Hand/troweling remains the most widely used application method, reflecting its suitability for localized and complex repair areas, whereas structural grade mortars account for the majority share due to emphasis on load-bearing restoration.

Building and carpark infrastructure represents the largest end-use segment, driven by dense urban construction and continuous maintenance needs. Increasing adoption of pre-engineered repair systems and performance-focused materials is further improving consistency, durability, and execution efficiency across repair applications globally.

Key Takeaways

- The global concrete repair mortars market was valued at USD 2.3 billion in 2025.

- The global concrete repair mortars market is projected to grow at a CAGR of 7.6% and is estimated to reach USD 4.8 billion by 2035.

- On the basis of product type, polymer-modified cementitious (PMC) mortars dominated the market, constituting 65.4% of the total market share.

- Based on the end-uses of the concrete repair mortars, building & carparks led the market, comprising 40.9% of the total market.

- Among the grades, structural concrete repair mortars held a major share of the market, accounting for around 70.2% of the revenue.

- In 2025, the Asia Pacific was the most dominant region in the concrete repair mortars market, accounting for 41.2% of the total global consumption.

Product Type Analysis

Polymer Modified Cementitious (PMC) Mortars Are a Prominent Segment in the Market.

Polymer Modified Cementitious (PMC) mortars represent the dominant product segment, accounting for 65.4% share, primarily due to their balanced performance characteristics and wide applicability across structural and non-structural repair works. These mortars combine cementitious binders with polymer additives that significantly enhance adhesion to existing concrete substrates, improve flexural strength, and reduce permeability against water and chloride ingress. Their relatively simple mixing and application process, compared to epoxy-based systems, makes them suitable for large-scale infrastructure rehabilitation, including bridges, parking structures, and road infrastructure.

PMC mortars also offer cost efficiency while maintaining adequate durability under moderate to severe exposure conditions. Their compatibility with hand, trowel, and spray application methods further supports adoption across varied field conditions. Additionally, compliance with standardized repair specifications and ease of integration into conventional construction practices reinforce their preference among contractors and infrastructure maintenance authorities globally.

Method Analysis

Hand/Troweling Dominated the Concrete Repair Mortars Market.

Hand/Troweling accounts for 45.6% share, making it the dominant application method in the concrete repair mortars market due to its versatility and suitability for localized repair works. This method is widely preferred for patch repairs, surface restoration, and structural touch-up applications where precision and controlled material placement are essential. It allows direct manual application onto vertical, overhead, and irregular concrete surfaces, ensuring strong bonding with the substrate when proper surface preparation is carried out.

Hand/troweling is particularly effective in confined or hard-to-access areas such as beams, columns, tunnels, and parking structures where mechanized application is not feasible. The method requires minimal equipment, reducing operational complexity and enabling cost-efficient execution across small to medium-scale repair projects. Its widespread use is further supported by compatibility with polymer-modified cementitious mortars, which offer improved workability and reduced sagging during application, enhancing overall repair quality and durability under varied field conditions.

Grade Analysis

Structural Concrete Repair Mortars Held Major Share of the Market.

Structural grade repair mortars account for 70.2% share, making them the dominant segment due to their critical role in restoring load-bearing capacity and ensuring long-term safety of deteriorated concrete structures. These mortars are specifically engineered to achieve high compressive strength, strong bond adhesion with existing concrete, and enhanced resistance to environmental stressors such as chloride ingress, carbonation, and freeze-thaw cycles.

They are extensively used in bridges, tunnels, industrial structures, high-rise buildings, and marine infrastructure where structural integrity is essential. Increasing aging infrastructure and stricter safety regulations have reinforced the demand for materials capable of restoring original design performance rather than merely providing surface-level repairs. Structural mortars are also compatible with various application methods, including troweling, spraying, and pouring, enabling flexibility across diverse rehabilitation scenarios. Their ability to extend service life and reduce the need for full structural replacement further strengthens their dominance in global repair and rehabilitation activities.

End Use Analysis

Concrete Repair Mortars Are Mostly Utilized for the Building & Carparks.

Building & Carparks account for 40.9% share, making it the dominant end-use segment in the concrete repair mortars market due to the high concentration of reinforced concrete structures in urban environments. These assets are subject to continuous load cycles, moisture exposure, and carbonation, leading to frequent deterioration in slabs, columns, beams, and parking decks. Repair mortars are extensively used for spall repair, crack filling, and surface restoration to maintain structural integrity and extend service life without major reconstruction.

Rapid urbanization and vertical construction growth have increased the number of multi-storey buildings and underground/above-ground parking facilities requiring periodic maintenance. The segment also benefits from relatively smaller-scale, repetitive repair requirements that favor cost-effective polymer-modified cementitious systems. Additionally, facility management practices in commercial and residential complexes emphasize preventive maintenance, further driving consistent demand for repair mortars in building envelopes and parking structures across developed and emerging urban centers globally.

Key Market Segments

By Product Type

- Polymer Modified Cementitious (PMC) Mortars

- Epoxy-Based Mortars

By Method

- Hand/Troweling

- Pouring

- Spraying

By Grade

- Structural

- Non-Structural

By End-Use

- Building & Carparks

- Road Infrastructure

- Utility

- Marine

Drivers

Deteriorating Infrastructure Assets Accelerate the Demand for Repair Solutions.

Aging infrastructure across global transportation and utility networks has created sustained demand for concrete repair mortars as a critical rehabilitation material, particularly in reinforced concrete bridges, highways, and public utilities.

According to the Federal Highway Administration (FHWA), reinforced concrete bridge deterioration in the United States is strongly influenced by long-term exposure to de-icing salts, leading to corrosion of reinforcement and progressive loss of structural integrity over time. Similarly, large-scale bridge inventory assessments indicate that a significant portion of structures are approaching or have exceeded their original design service life, requiring continuous repair interventions rather than replacement-based strategies.

Empirical bridge condition studies covering multi-decade inspection datasets show that certain reinforced and prestressed concrete bridge categories experience accelerated deterioration within the early to mid-life cycle, reinforcing the need for periodic rehabilitation planning rather than reactive maintenance approaches. In parallel, documented structural failures, such as the Morandi Bridge collapse in Italy, have highlighted the consequences of delayed maintenance and insufficient rehabilitation investment, reinforcing the urgency of systematic intervention practices.

Government and engineering agency publications consistently note that deterioration mechanisms—including cracking, chloride ingress, carbonation, and fatigue loading—intensify under increasing traffic volumes and environmental stressors, accelerating maintenance backlogs and widening repair demand. These conditions directly support higher utilization of polymer-modified and epoxy-based repair mortars for localized strengthening, spall repair, and durability restoration in structurally compromised assets.

Restraints

Performance Variability Arising from On-Site Application Conditions May Limit Market Adoption.

Performance of concrete repair mortars is strongly influenced by field execution conditions, where deviations from controlled laboratory parameters often translate into measurable differences in durability outcomes. Studies on cement-based repair systems indicate that curing environment alone can significantly alter hardened performance, with variations in relative humidity (e.g., 60%–100% RH ranges) affecting pore structure development, transport properties, and permeability indices of mortars used for rehabilitation applications. Laboratory–field correlation analyses further show that surface quality and in-situ permeability indicators such as gas permeability and water absorption exhibit strong dependence on curing regime and on-site exposure conditions, reinforcing the sensitivity of repair performance to installation practices.

In practice, improper substrate preparation, inconsistent moisture conditioning, and uncontrolled drying can lead to inadequate bond formation between repair mortar and existing concrete, which is a primary mechanism behind delamination and early-age cracking failures identified in repair specifications guidance documents. Variability in mixing water content and application timing further intensifies performance dispersion, as even small deviations in water–binder ratio can significantly alter compressive strength and shrinkage behavior. Additionally, field studies highlight that compatibility between repair material and parent concrete must be carefully controlled, since mismatches in transport properties and stiffness contribute to differential movement under service loading conditions.

Collectively, these quantified sensitivities underline that real-world performance of repair mortars is not solely material-dependent but strongly governed by execution discipline, environmental exposure during placement, and quality assurance consistency across repair sites.

Opportunity

Shift Toward High-Performance and Pre-Engineered Repair Systems Enhance Market Potential.

Pre-engineered repair mortar systems—comprising factory-controlled polymer-modified cementitious and epoxy-based formulations—are increasingly being specified in structured rehabilitation works due to their standardized performance parameters and reduced dependency on field proportioning. Technical specifications issued under infrastructure authorities emphasize that polymer-modified cementitious repair mortars are designed to deliver compressive strength typically in the range of 20–50 MPa with controlled shrinkage and bond strength exceeding 1.0 MPa to existing concrete substrates, ensuring predictable structural compatibility in repair zones.

Engineering guidelines for reinforced concrete rehabilitation highlight that pre-bagged repair mortars are preferred over site-batched mixes due to reduced variability in polymer dosage and water–cement ratio control, which directly influences adhesion, permeability, and long-term durability performance under service exposure conditions. In parallel, specifications for structural repair systems commonly require compressive strengths exceeding 35 MPa at early curing stages and dimensional stability limits defined under standardized testing protocols such as ASTM C157, reinforcing the shift toward engineered formulations with verified performance consistency.

Field application guidelines further indicate that machine-applied or pre-packaged systems reduce onsite mixing errors, particularly in vertical and overhead repairs, where improper water addition or curing practices can significantly alter material performance. These controlled systems are increasingly used in infrastructure restoration works such as bridge soffit repairs, industrial flooring rehabilitation, and marine structure resurfacing, where repeatable mechanical properties and rapid strength gain are essential for minimizing operational downtime.

Trends

Shift Toward High-Performance and Pre-Engineered Repair Systems.

A noticeable shift toward pre-engineered and high-performance repair mortar systems is increasingly embedded within formal specification frameworks for concrete rehabilitation works. Public infrastructure specifications, such as those aligned with ACI 318 and ACI 301, emphasize controlled material performance and standardized testing of repair mortars, including compressive strength verification using ASTM C109 methods for hydraulic cement mortars, reinforcing the preference for predictable, lab-validated material behavior in field applications. This structured specification approach supports the growing use of factory-prepared, polymer-modified, and epoxy-based formulations designed to reduce variability associated with site batching.

Engineering guidance for concrete restoration under internationally referenced repair principles (EN 1504 series) further formalizes the use of hand-applied, sprayed, or recast mortars under defined performance classes, where durability, adhesion, and load-bearing restoration requirements are explicitly tested and certified before deployment. Such codified requirements are encouraging substitution of conventional site-mixed mortars with pre-bagged systems that ensure consistent binder composition, controlled water demand, and uniform admixture distribution.

Field-level adoption is also influenced by operational efficiency requirements in infrastructure maintenance, where rapid return-to-service constraints in transport corridors and industrial assets favor fast-setting engineered mortars. These systems help minimize variability in curing behavior under fluctuating temperature and humidity conditions, improving reliability in bridge decks, parking structures, and utility repairs.

Geopolitical Impact Analysis

Geopolitical Disruptions and Supply Chain Reconfiguration in Concrete Repair Mortar Supply Networks.

Geopolitical tensions have increasingly translated into structural stress across construction material supply networks, directly influencing the availability, pricing stability, and logistics efficiency of cementitious repair systems used in concrete rehabilitation. Restrictions arising from trade sanctions, regional conflicts, and export controls on industrial inputs have contributed to intermittent shortages of key raw materials such as clinker additives, polymer resins, and epoxy precursors, all of which are critical to repair mortar formulations. Recent public trade monitoring has recorded a sharp rise in restrictive measures on critical inputs globally, with more than 200 import and export restrictions on strategic materials enacted within a single year, reflecting tightening material flows across borders.

Maritime disruptions and rerouting of shipping lanes have also extended lead times for bulk construction materials, with some logistics corridors experiencing transit extensions of over 10–14 days due to the avoidance of high-risk maritime zones. This has increased reliance on regional sourcing and stockpiling strategies by infrastructure agencies to maintain continuity in repair works. In parallel, fuel price volatility linked to energy corridor instability has elevated transportation costs, indirectly affecting the landed prices of packaged repair mortars used in bridge, tunnel, and utility rehabilitation projects.

Public infrastructure agencies have reported procurement delays and phased execution of maintenance programs where imported specialized repair systems are involved, particularly for epoxy-based and high-performance polymer-modified mortars. These disruptions have reinforced material substitution tendencies toward locally produced formulations and accelerated the adoption of multi-sourced procurement frameworks to reduce exposure to single-region dependency risks.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Concrete Repair Mortars Market.

Asia Pacific remains the dominant regional market for concrete repair mortars, supported by extensive infrastructure stock, accelerated urban expansion, and large-scale rehabilitation programs across transport and utility assets. China alone represents a significant proportion of regional consumption, driven by the continuous redevelopment of bridges, highways, and urban transit systems, alongside coastal protection and industrial upgrades.

Government-led infrastructure investment programs in countries such as India, China, Japan, and South Korea are systematically prioritizing lifecycle extension of civil assets, particularly in metro rail corridors, expressways, and water management systems. FHWA-style infrastructure condition assessments and analogous regional agency reports highlight that reinforced concrete structures in heavily trafficked corridors experience accelerated deterioration from chloride ingress, carbonation, and fatigue loading, necessitating recurring repair interventions rather than replacement-based solutions.

Urban density and extreme climatic exposure further intensify maintenance cycles, particularly in coastal megacities where marine exposure and humidity-driven corrosion are prevalent. These conditions sustain consistent application of polymer-modified and epoxy-based repair mortars across structural, non-structural, and surface restoration applications in the region.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of concrete repair mortars strengthen their competitive positioning through continuous product innovation, particularly by developing polymer-modified and epoxy-based formulations that offer improved adhesion, reduced shrinkage, and enhanced resistance to chemical and chloride exposure. Significant emphasis is placed on expanding pre-engineered and ready-to-use systems to minimize site variability and improve application consistency across diverse field conditions.

Many producers invest in in-house testing facilities to validate compressive strength, bond performance, and durability parameters before commercialization. Strategic partnerships with construction contractors and infrastructure agencies help secure specification-level approvals in bridge, tunnel, and utility rehabilitation projects. Companies also focus on localized manufacturing and regional supply chains to reduce lead times and raw material dependency risks. Additionally, technical service support, on-site training programs, and specification assistance for engineers and applicators are used to strengthen adoption and long-term customer engagement.

The Major Players in The Industry

- Adhesives Technology Corporation (ATC)

- ARDEX GmbH

- ChemCo Systems

- Flexcrete Technologies Ltd

- Heidelberg Materials (Hanson Repair)

- Kryton International Inc.

- MAPEI S.p.A.

- MC-Bauchemie

- Pidilite Industries Ltd

- Polycote

- Remmers GmbH

- Saint-Gobain

- Sika AG

- Tarmac

- The Euclid Chemical Company

- R. Meadows Inc.

- Other Key Players

Report Scope

Report Features Description Market Value (2025) US$2.3 Bn Forecast Revenue (2035) US$4.8 Bn CAGR (2025-2035) 7.6% Base Year for Estimation 2025 Historic Period 2021-2024 Forecast Period 2025-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Polymer Modified Cementitious (PMC) Mortars and Epoxy Based Mortars), By Method (Hand/Troweling, Pouring, and Spraying), By Grade (Structural and Non-Structural), By End Use (Building & Carparks, Road Infrastructure, Utility, and Marine) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape Adhesives Technology Corporation (ATC), ARDEX GmbH, ChemCo Systems, Flexcrete Technologies Ltd, Heidelberg Materials (Hanson Repair), Kryton International Inc., MAPEI S.p.A., MC-Bauchemie, Pidilite Industries Ltd, Polycote, Remmers GmbH, Saint-Gobain, Sika AG, Tarmac, The Euclid Chemical Company, W. R. Meadows Inc., and Other Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Concrete Repair Mortars MarketPublished date: May 2026add_shopping_cartBuy Now get_appDownload Sample

Concrete Repair Mortars MarketPublished date: May 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Adhesives Technology Corporation (ATC)

- ARDEX GmbH

- ChemCo Systems

- Flexcrete Technologies Ltd

- Heidelberg Materials (Hanson Repair)

- Kryton International Inc.

- MAPEI S.p.A.

- MC-Bauchemie

- Pidilite Industries Ltd

- Polycote

- Remmers GmbH

- Saint-Gobain

- Sika AG

- Tarmac

- The Euclid Chemical Company

- R. Meadows Inc.

- Other Key Players

Our Clients

- 185724

- May 2026